Last Updated on May 21, 2026 11:43 pm by Maxwell Aliang’ana

Debt is a weighty burden. The burden of debt—whether in the form of a student loan, credit card debt, medical debt, or car loans—can impact your finances, as well as your mental well-being, your relationships, and your plans for the future. Once you’ve made the decision to take a stand, there are two methods that seem to be the most popular: the debt snowball and the debt avalanche. In this article I will discuss both strategies in detail, weigh their pros and cons, and give you the answer as to which course of action is likely to be the best one for you to take in order to reach the debt free lifestyle.

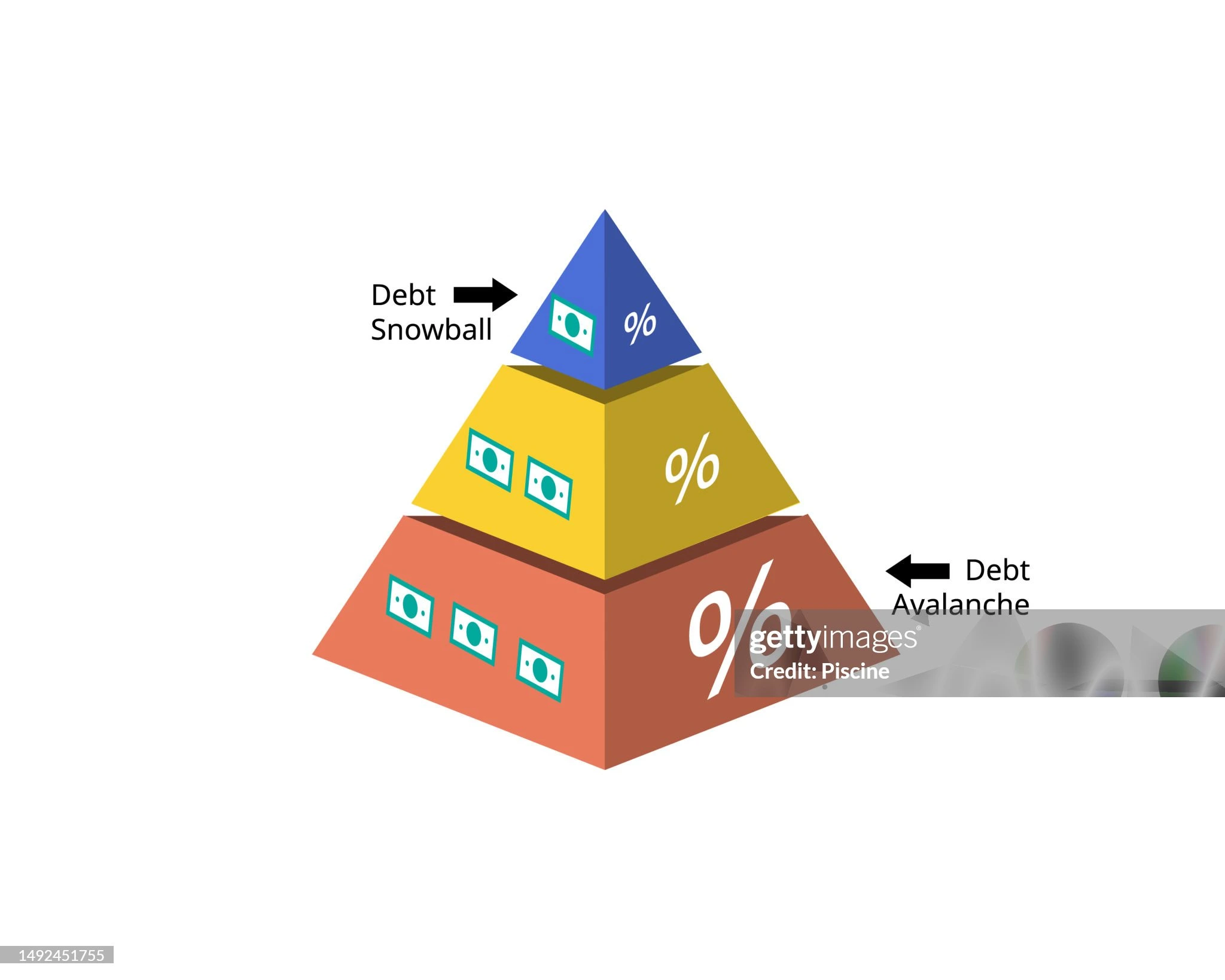

Understanding the Debt Snowball Method

The debt snowball method was popularized by the personal finance expert Dave Ramsey, and is named after a little snowball that slowly rolls to become bigger. According to this method, you’ll order your debts from lowest to highest balance without considering interest rates. You pay minimum payments on all of your debts, but you pay as much as you can towards your smallest debt on your list. When the smallest one is paid off, you use the amount of debt you were paying on the smallest and add it to the minimum amount you were paying on the next smallest debt. This has a snowball effect, whereby your debt repayment towards the next debt increases each time and thus speeds up your repayment process over time. For instance, you might have a medical bill of $500, a credit card debt of $2000 and a student loan of $15000. With the snowball approach, you make the smallest minimum payments on all bills except the 500 dollar bill that you attack first. This little amount is gone after a month or two. You are now feeling good about yourself and are inspired to do more with the 2K credit card, since now you have some money to spare from the hospital bill to go into the credit card, which has the same payment amount.

The Psychological Power of the Debt Snowball

The main reason for the debt snowball is not a mathematical one, but more of a behavioral one. Personal finance is not financial, it’s personal. Man is not a calculating machine. Emotion, momentum, and seeing results are what drives us. If you’re drowning in debt, the road to pay off those debts can seem so long. It’s frustrating to have a $15,000 student loan and not know how to move forward. The debt snowball provides you with some fast wins. It is rewarding, and gives you a sense of accomplishment, to pay off a small debt in the first month or two, and then a larger one in the next. This little win releases dopamine, the chemical that is related to reward and motivation. You feel good, so you go on. The more you pay off a debt, the more your financial condition improves, and the more you feel this way, the more you pay off a debt. This feeling is backed up by financial behaviour research. While the avalanche method was more paper money efficient, a study from the Kellogg School of Management revealed that debtors who employed the snowball method were more likely to be able to save their debts using the method than those who used the avalanche method. The researchers found that it was the sense of progress and not the mathematical optimum that helped predict success. As it gets people’s confidence when they see accounts being closed and balances are going down to zero. They start to think that they can really be debt free. This belief turns into a self-fulfilling prophecy.

The Mathematical Weakness of the Debt Snowball

But critics of the debt snowball are right that the debt snowball isn’t mathematically efficient. You could pay a lot more in the end by neglecting interest rates. There may be a small debt with no interest and a large debt with a twenty five per cent rate of interest that can be paid off before the smaller debt. During that time that you’re celebrating you’ve eliminated that small zero interest debt, the high interest debt will continue to compound and you’ll end up paying hundreds or thousands of additional dollars in interest charges. Emotionally the snowball is a pleasant feeling, but it may be costly on a monetary basis. Let’s think of a realistic example. You have a $500 medical bill that is paying no interest, a $3,000 credit card bill at 18 percent and a $10,000 student loan bill at 5 percent. The snowball method is the same, but the order of payments is medical expense, credit card, student loan. First, you pay off the credit card since it has the highest interest rate as it is the most over-laden credit card. The snowball may end up costing you a few hundred dollars in interest over the course of your debt repayment plan. If you have a great deal of debt, the difference can be in the thousands of dollars, if you have a very high interest rate.

Understanding the Debt Avalanche Method

The debt avalanche method is just the opposite. Debts are not sorted by amount of debt, but by interest rate, highest to lowest. Your regular payments are made on all the debts, and any surplus of the amount you owe is applied to debts with the highest interest rates first. After this debt is paid, the money paid towards it is being rolled into the debt with the next highest interest rate, and so on. Credit cards are all the way “gravity” grows and falls on to the debt you owe, but the important image is mathematical gravity. The worst debts to have are high interest debts because they drag you down the fastest, so you pay them off first to prevent the damage. Again with the same scenario, the avalanche strategy would pay off the three-thousand-dollar credit card at 18% and the five hundred dollar medical bill at zero%. In terms of math, this is better. For every dollar paid on the credit card, you’ll owe eighteen cents a year in credit card interest. Since the interest rate is 0% you are not paying any interest for each dollar that you pay towards the medical bill. If you’re paying the same monthly amount to pay the debt, the avalanche method will reduce the total amount of interest that you pay, and will shorten your debt payoff period by calendar month.

The Mathematical Power of the Debt Avalanche

If only numbers were considered, the debt avalanche would be the better option. It is simple math. The higher the interest rates, the more it’s going to cost you per dollar of borrowed capital, and the sooner you pay down those rates, the less you’ll have to pay off on your debt as a whole. The avalanche method is almost always recommended by financial advisors who deal with number and not emotions as it’s the cheaper way to pay off debt. The savings can be significant over a number of years of debt payments. If a person has $20,000 in credit card debt at 20 percent interest, and $40,000 in student loans at six percent, paying off the student loans first, at the lower interest rate, may cost a few thousand dollars more for them. The avalanche method can save you some time in eliminating your debt, too. You’ll be paying off the highest interest loans first, so that more of your payments will go towards the principal balance. This translates to deducting more of the principal amount in each payment, thereby speeding up the whole process. The avalanche is definitely better if you’re only trying to figure out how to save up to repay your debt as soon as possible and how to avoid wasting any money on interest.

The Behavioral Weakness of the Debt Avalanche

The issue with the avalanche method is that it demands self-control and patience that many of the debtors don’t have. It could be several months or many years before a person can pay off a high interest credit card, particularly if they owe a lot of money on the credit card. That is when you will barely see any changes in your progress. You will be paying after each payment and the amount will be slowly reduced. The other little debts that are left behind will taunt you with their very existence. This gradual improvement can be discouraging to an already hopeless person. Since there are no quick wins, you’re going to get demotivated and you’ll give up. A plan that’s optimal in math, but abandoned after the six-month time period is worse than a slightly suboptimal plan, which is followed through. The avalanche system also does not consider the psychological benefits of “avalanching” your bills. Once you pay off one of your debts in the snowball plan, you have one less bill, one debt, and one less day when you pay a bill. This has taken away mental burden and cost anxiety. With the avalanche method, you may be able to pay on a debt you owe for years without paying off any of the others if you have one debt with a very high interest rate and also have a very large balance on the other debt. You feel like you are making maths-optimally good progress, but you are still as trapped as at the start.

Which Strategy Is Right for You

Well, it’s all about you and your approach to spending. The debt avalanche is for those who are disciplined and self-motivated enough to avoid steady rewards and are numbers-oriented. You’ll save money, save time and you won’t be tempted to give up on your plan because it seems slow. A debt snowball is more effective for you if you are a motivated person, you have tried budgeting, you have been overwhelmed by your debt, or you have a large amount of debt. The wins will help to establish a sense of accomplishment and success. A slower and more costly plan, but one that you will follow is much better than a faster and cheaper plan that you will not finish. There’s also an in-between. Other debtors, however, will take the opposite strategy and settle the highest interest debt first, if they have any debt with a very low balance that can be paid off in a month or two. They use the small debts to give them a psychological benefit and then use the avalanche method. Others apply the snowball approach to credit cards and consumer debt, and have a different approach to student loans or mortgages. Most important is to choose a system and stick with it. The very nature of analysis paralysis means you’re spending more time than any suboptimal strategy will.

Final Thoughts on Freedom From Debt

The debt snowball and the debt avalanche have helped to graduate many debt free students. The snowball has been doing its job with those who were needing emotional energy to carry on. The avalanche has been a great tool for the people who optimized debt repayments. What the common denominator has got in all success stories is that they have made a decision to continue paying and to never spend more than they are making, as well as their refusal to take on new debt in order to pay off old debt. You can come in as a snowball or avalanche, but the end result is the same. The best approach is the one that you are going to be able to follow until you’ve paid off your last debt and the burden is no longer on your shoulders.

Discover more from Kenya Financial Updates

Subscribe to get the latest posts sent to your email.

{kind=link}

{kind=link}