Last Updated on May 18, 2026 8:49 am by Maxwell Aliang’ana

When Debt Becomes a Heavy Load

Debt is not bad. The well-designed loan can purchase you land, support your kid’s school fees, or even assist you in starting a small business. However, when debts are accrued from several lenders, each employing a separate interest rate, even responsible borrowers can find themselves feeling overwhelmed. Will Kenyan wage earners benefit from this? This article offers a wholly honest and local perspective on debt consolidation, when it works and when it doesn’t, and how to do it safely.

What Is Debt Consolidation Exactly?

Debt Consolidation is a process of using a new loan which is larger in amount and is used directly to pay off a number of smaller loans. Instead of repaying six different lenders each month, you repay just one. There is an easy to understand theory behind it. When you have a new loan with a lower interest rate than the average of your old loans, then you are saving money. The longer the loan term, the lower your monthly payments will be and more manageable. Suppose that you have Ksh 20,000 due on Fuliza at 8% per month, Ksh 30,000 due on a digital loan at 10% per month and Ksh 50,000 due on a Sacco at 2% per month. Three separate payments are being made. All three would be closed if they were consolidated under a bank loan of KSh 100,000 at 3% per month from a well-regulated bank or lender. Then you pay KSh 3000 monthly interest and principal. Your financial life is made easy. This is the assurance.

Why Consolidation Is Tempting

The credit market in Kenya is uniquely attractive for debt consolidation in a few regards. First, there are so many digital lenders that it’s extremely easy to build up small, high interest loans. Fuliza, Zenka, Tala and Branch provide instant loans at an effective interest rate that can be more than 30 per month if all fees are added in. A person can download three apps and take KSh 15,000 in debt in 10 minutes with no interaction with a human being. Second, there is a tendency for Kenya to borrow from both formal and informal sources. You may have loans to a bank, a Sacco, a digital lender, a shop and a relative. They are all different and their collection methods are different. Thirdly, the pressure of several pay-back dates is a reality. Late payments can cause late fees, calls for harassment and CRB listing. Consolidation offers the psychological relief of a single deadline.

The Benefits: When Consolidation Makes Sense

Debt consolidation will make sense in three particular conditions. The first is when you can get a much lower interest rate. For example, a Sacco loan may have an interest charged from 1%-2% per month on the outstanding balance. The interest rate of a bank personal loan can be as high as 13% to 18% per year. Unsecured digital loans, on the other hand, can have effective monthly rates ranging from 8% to 15% . If you have a digital debt of KSh 50,000, payable at 10% p.m, take a bank loan at 14% p.a, the interest you pay monthly will drop from KSh 5,000 to KSh 583. This means that you save KSh 4,417 monthly. The second is when you’re having cash flow issues but you are not really insolvent. If an individual’s total debt payments are KSh 45,000, and they make KSh 60,000, they are drowning. You get breathing room when you consolidate your loans at a reduced payment of KSh 30,000. The third situation is when there’s no prepayment penalties on the consolidation loan and you agree to refrain from adding additional debt. If you roll over the balances and then proceed to add more right away, you’ve only made things worse, not better.

The Hidden Dangers: When Consolidation Backfires

There is a lesson to be learned from every debt consolidation success story, and a warning from every debt consolidation failure story. The biggest threat is that of having a long time frame to pay back, which means paying more interest in the long run. The interest costs on a KSh 100,000 loan for 15% per annum repayable over 2 years is about KSh 16,000. The interest paid for the same debt five years is nearly KSh 42,000. This means that you will have lower monthly payments, but you will end up paying more in the long term. The second risk is consolidating your debts on unsecured loans that have a higher rate of interest than some of your other loans. Your Sacco loan is costing you 1% per month, and your consolidation loan is costing you 3% per month, it’s mathematically inapropriate to consolidate the Sacco loan into the new loan. The bad debt is the one that you should consolidate and not the cheap debt.

The third and most sinister is behavioural. The number of borrowers who consolidate their debt, get relieved and then start borrowing again. They view the consolidation as an opportunity to spend. They have the consolidation loan, new Fuliza and digital loans and new shop credits within 6 months. They’re now twice as in debt as they were. This is the debt consolidation trap, according to financial counsellors. If you are not making a change in your spending habits, then consolidation is just moving the chairs around on the Titanic!.

How to Consolidate Safely in Kenya

The following is a list of steps to follow if you have already determined that consolidation may be an ideal solution for you. First, you should make a list of all debts that you have, including the financial institution where you are taking the loan from, the amount outstanding, interest rate and any fees. Consider unpaid debts to friends and family, those emotional debts which are often overlooked. Second, work out the effective annual interest rate for each debt. Digital lenders tend to mention daily/monthly rates. Multiply these rates by 12 to convert the monthly rates to annual rates. If, for instance, you have 8 per cent per month, then it translates to 96 per cent per year. This is a shocking number that will allow you to determine which debts you need to consolidate first. Third, seek a reputable lender who will offer a consolidation loan. There are several possibilities in Kenya. KCB M-Pesa provides loans of up to Ksh 1 million, with a monthly interest rate of 8.64%, the interest is calculated on a reducing basis. NCBA’s Loop offers personal loans with a flexible repayment option. Many Saccos provide consolidation loans to their members with an interest rate of 1% – 2% per month. Both equity Bank and Co-operative Bank offer personal loan products which can be used for consolidation. Fourth, as soon as you receive the consolidation loan, pay off the debts targeted. Never leave money in your account for one day or longer. Its allure to spend money is irresistible. Last but not least, close the accounts that you have paid off. Remove digital lending apps. Cut up the shop credit cards. Prepare obstacles to reborrowing.

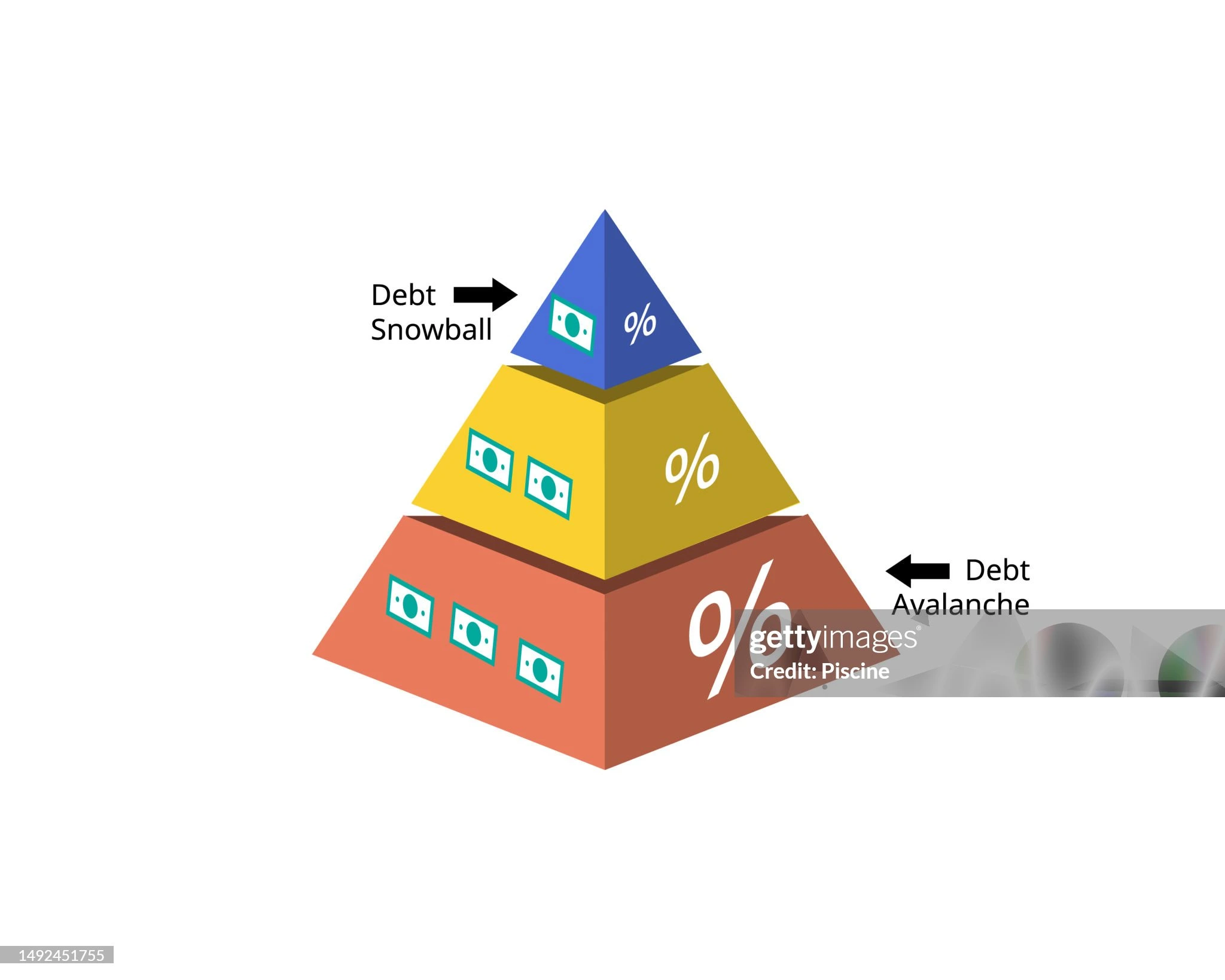

The Alternative: DIY Debt Snowball Without a New Loan

There are other alternatives to debt consolidation. In Kenya, many people manage to do it all on their own and that is what is known as the debt snowball. This way, you don’t borrow an additional loan. Rather, you pay all the minimum payments for all your debts, and then pay extra at the smallest debt possible. Once the smallest loan is paid off, the loan payment goes towards the next smallest loan. The method is successful because of psychology and not mathematics. It’s satisfying to clear a small debt and make progress and to give yourself a sense of momentum. For instance, if you have Ksh 3,000 balance on Fuliza, Ksh 15,000 digital loan and Ksh 50,000 Sacco loan, you can raid on Fuliza first. You don’t go out to eat for 2 weeks, sell an item that you didn’t use and then you clear it. As one debt is cleared another debt will follow. There is no need for consolidation loan and that you will not risk further debt.

The Math: A Worked Kenyan Example

Let’s take James, a Nairobi salesman who makes KSh 70,000 net salary monthly. He has four debts. Fuliza: Ksh 8000 with an effective interest rate of 10% per month. Tala loan: KSh 12,000 at 9% per month. Sacco loan: KSh 40,000 at 2% per month. Shop credit: Ksh. 5,000 with no interest, but harming the relationship with the retailer. His monthly interest for Fuliza is approximately Ksh 800, Tala is Ksh 1080 and the Sacco is Ksh 800, and Interest only totals Ksh 2680 per month. A bank is asking James to consolidate his debts into a single loan of KSh 65 000 payable over 2 years at a rate of 14% per annum or about 1.17% per month. He pays off about Ksh 760 monthly interest on his new loan. He saves Ksh 1,920 Interest monthly. In addition, his new monthly principal and interest payments are approximately Ksh 3100 while his previous total minimum payments were approximately Ksh 8000 per month. Now he has an additional saving of KSh 4,900 per month or expenses. The word consolidation is very effective for James, as he has agreed to not take out any more loans. If he fails to keep his promise, he will be worse off in 6 months.

When to Say No to Consolidation

If the new loan has a higher interest rate than the one you currently have, don’t combine. When you haven’t dealt with spending patterns that got you into debt, then don’t consolidate. Suppose you’re just looking to lower your monthly payment without a savings or debt payoff plan, then don’t apply the funds to consolidate. Also, do not consolidate with the only lenders who will approve being predatory digital apps. An example of this is borrowing from a loan shark to pay off other loans, which is similar to jumping out of the frying pan into the fire.

Conclusion: Consolidation Is a Tool, Not a Miracle

It’s not all bad or all good—debt consolidation itself is a monetary instrument. When used properly, it can reduce your interest payments, make your life easier and provide you with breathing space. If it’s not used properly, it can prolong your debt, raise the overall interest you are paying and allow you to have even poorer borrowing practices. It’s not whether or not consolidation is a good idea in general. Whether it is worth it for you in your circumstances, your debts, your behaviour. Make a list of your debts. Work out your interest charges. Shop for consolidation loans among authorised banks and Saccos. Most importantly, put in place a plan to change the behaviors that led you to this place. While a well-designed loan can help a borrower, a borrower who is unwilling to change cannot be saved by any loan, however well it is designed. However, if a borrower is willing to make a change, consolidation can be the first step towards financial freedom.

Discover more from Kenya Financial Updates

Subscribe to get the latest posts sent to your email.

{kind=link}

{kind=link}