Last Updated on May 19, 2026 1:01 pm by Maxwell Aliang’ana

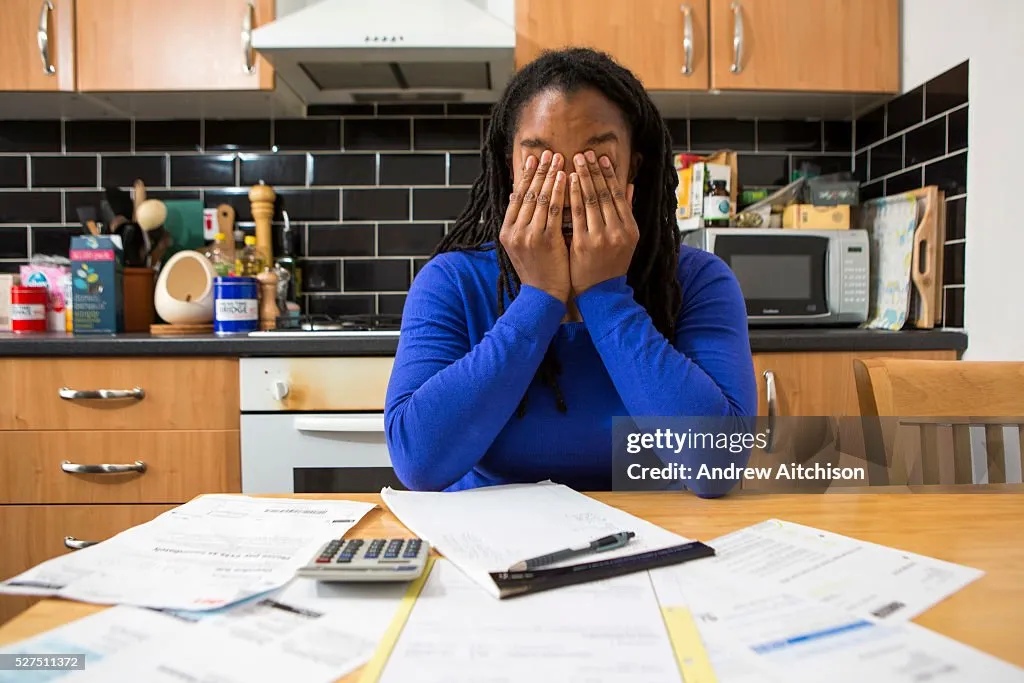

The Silent Weight of Debt

Most of the time, when Kenyans talk about debt, they are talking about numbers: interest rates, repayment periods, credit scores, CRB listings, etc. However, behind the numbers and the reminders for payment lies the darker side of things which not many people talk about. Debt is more than just a financial matter. It is a mental trauma that leads to poor mental health, reduces productivity and weakens relationships. It involves many nights in the month spent figuring out how to pay off a Fuliza. Every time you get a call, you are worried about whether it’s from a lender. The embarrassment of taking a loan from a friend and paying the interest for an earlier loan. The embarrassment of borrowing from a friend and paying interest to the previous loan. These are not the costs of the debt. They are at the heart of the trapping experience. This article examines the impact of debt on mental wellbeing and productivity of borrowers in Kenya, why borrowers are suffering in silence and what you can do to get out of debt.

The Psychology of Debt: More Than Just Money

There is a strong connection between money and emotions. When you owe money, you are not simply experiencing a cash flow problem. The feeling of losing control. The sense of out-of-control. Psycho stress of debt is as intense as physical stress and is known to activate the same stress responses in the brain. When someone is financially strained, their fear and anxiety centers are over-activated, the amygdala, which is part of the brain. This is not about the weakness. It is biology. The impact is greater for the Kenyan borrowers because our credit market is such that we have a credit market with concentrated borrowers. Digital lenders are the ones that provide instant loans at very high interest rates. Sacco deductions are cut directly from one’s salary. Daily interest, compounded upon Shylocks’ head, adds to the stress with each dawn. What you get is a long-term state of mild anxiety, which takes a toll on mental health after months and years.

Anxiety: The Constant Companion of the Indebted

The top mental health impact of debt is anxiety. Anxiety is not a state of worry. It’s an ever-present, pervasive, and debilitating fear that disrupts your life. The debtor’s anxiety can be expressed in a variety of ways. It’s three in the morning and you can’t sleep – you’re in your mind recapping your finances. Avoid taking calls from your phone from a lender and/or a creditor because you are afraid of them. Every time you check your M-Pesa balance you experience a knot in your stomach. When you think about money, you have physical responses such as headaches, tense muscles and a quickened heartbeat. Family responsibilities and ‘black tax’ in Kenya can create an extra burden of financial responsibility which can leave people feeling overwhelmed by anxiety. In 2020, the Kenya National Bureau of Statistics revealed that almost 40 percent of individuals that had indicated they were in high debt were also experiencing moderate to severe anxiety. The two conditions go hand in hand.

Depression: When Debt Becomes Hopelessness

Anxiety is fear of what may occur, depression is the belief that things will never improve. A person’s sense of depression is caused by chronic debt if he or she feels as if there is no way out of the debt. There’s something going haywire with the Math things. You figure out how much money you make, then subtract your debt payments and you simply don’t have money left to save, to pay an emergency, or to have fun! The situation doesn’t change month after month. Hope fades. Depression sets in. Symptoms range from persistent sadness, inappropriate increase or decrease in appetite or eating, changes in sleep patterns, and, in very severe cases, thoughts of self harm or suicide. In Kenya, some borrowers have even committed their own suicide when they were unable to pay off their debts, or were being harassed by the lenders. The same year a lecturer in a university in Nairobi, Kenya, committed suicide due to pressure from digital loan providers who reached out to fellow university staff and students. He spoke about the troubles of shame and hopelessness in his suicide note. His debt was KSh 48,000. It was a trifling sum. There was no psychological load.

Shame and Stigma: Why Borrowers Suffer in Silence

The shame is one of the most vicious forms of mental illness that occurs with the debt problem. Self-sufficiency and provider attitude are very important in Kenyan culture. A parent that is unable to send his children to school is a failure. A woman who feels she has to borrow money to feed people feels she has failed them. This embarrassment hinders people from getting help. You don’t let your friends know that you are in debt, because you’re afraid of being judged. If you don’t see a counsellor because you think your issue is money rather than mental health, it is not a counsellor’s duty to address the financial aspect. You suffer alone. The irony is that the place of shame is in its secrecy. As soon as it is verbalized to a trusted person, some of the power is lost. However, the stigma associated with taking debt in Kenya is so great that many borrowers would rather suffer from panic attacks and sleepless nights than come out as being in debt. It is a silent that is lethal.

Productivity Loss: How Debt Follows You to Work

Debt doesn’t remain within the confines of the household. It goes wherever you go—you go to the office, it goes to the office, you go to the workshop, it goes to the workshop, you go to the marketplace, it goes to the marketplace. The studies in cognitive science suggest that financial issues take a lot of your working memory. This is referred to as cognitive load in the Financial domain. If you’re constantly distracted by debt, you don’t have as much mental capacity working on the task at hand. There are more mistakes made. You forget instructions. Have difficulties focusing at meetings. Delays in task completion. This can be a missed deadline, a substandard performance appraisal and ultimately a loss of income to the Kenyan worker. The consequences are even more severe for the self-employed or a hustler. You can’t think about your customers’ needs when you’re working out a repayment plan for a loan. You’re in a hurry to make quick money and put out low quality work. Your reputation suffers. Your income is reduced even more. The debt grows. This is the productivity death spiral.

Presenteeism: Being at Work but Not Working

There is also another term which refers to absence in mind while being present in the body – presenteeism. Presenteeism is a common problem among indebted workers, and is not commonly measured by Kenyan employers. You’re at your desk but you’re not at your desk. You start your laptop but spend 30 minutes checking the M-Pesa transactions and balances of your loan. You go to a meeting but during it you start to work out how you will pay off a debt which is due tomorrow.You attend a meeting, but at the meeting you start to work out how you will pay off a debt that will be due tomorrow. Based on research in organisational psychology, the cost of presenteeism is said to be between two and three times the cost of absenteeism to the employer. The employee is available, but is doing little to nothing. Presenteeism makes the working person who is in debt to someone very miserable. You are at work and you feel you are trying. However, you’re not performing, and so your career isn’t moving forward. Promotions are not awarded. You are not paid any more. The debt remains.

Relationship Strain: Debt as a Relationship Killer

Whether you’re drowning in debt or just getting started, these tips can help you keep it from destroying your marriage. A borrower’s debt load isn’t the only thing that’s affected. It impacts all those around them. Particularly sensitive are romantic relationships. Money is always one of the number one reasons for divorce and the breakup of relationships, globally and in Kenya. One partner keeps the other partner in the dark about the debts, thus building up a breach of trust. The non-borrower is resentful, particularly if he or she has to make payments on debts that he or she did not incur. Intimacy suffers. You don’t go out for date nights because you don’t have any money. The relationship turns into a “transaction,” a “survival relationship” no longer a “relationship of connection. Kids aren’t spared of the impact, either. When parents are stressed about debt, they are not as patient, present, or likely to be as forgiving. A place of safety is another source of tension in a home. More often than not, debt will kill a family before a bank can.

The Physical Toll: Headaches, High Blood Pressure, and Insomnia

Mental health issues can’t be divorced from physical health. They are connected. Long-term stress from debt can cause physical changes that can be measured. One might say there is hardly anyone who is not suffering with insomnia among the severely indebted. You’re lying on your bed, but your mind is still counting. After 3 hrs of sleep you wake up tired. After weeks and months of not sleeping, your immune system is compromised. Increased illness. Your headaches start to occur every day, and are caused by the tension in your neck and shoulders. Blood pressure rises. Financial strain has been recognized as a risk factor for hypertension, heart disease and stroke. A score is maintained by the body. When you lie to yourself about something and say that you are coping with the debt, you lie to yourself. I’ll present the physical symptoms as proof.

Breaking the Cycle: What Borrowers Can Do

If you feel you can identify yourself in this description, the first thing you should hear is: You are not alone! Kenya’s tens of thousands of debtors suffer similar mental ailments as those of the nation’s debtors. The second is you can act, even during the repayment period. First, take the financial issue out of the psychological issue. It’s possible to work on mental health issues without paying off your debt. Seek professional help. There are many counselling services available in Kenya, including the Kenya Counselling and Psychological Association, which offer affordable services; additionally, some work place health care plans cover mental health services. Communicate with someone you can trust. The sense of shame you experience is NOT a sign of who you are and your worth. If it’s a symptom of a system that profits from your silence, what did you expect?

Now perform practical financial moves that also help to lighten the emotional burden. If it helps to lower the interest rate and decreases the amount of lenders calling, combine multiple loans into one. Discuss with creditors. Many lenders would prefer to get a smaller, steady payment, rather than go after the defaulting borrower. Shield No. of unlicensed lenders who are harassing. They don’t have any legal rights to collect any debt and you don’t have to put up with their abuse. Last but not least, come up with a reasonable repayment plan, rather than a heroic one. If you are only able to pay KSh 500 in a week for a debt, then pay that. It’s better to do something than to do nothing. Even if you make just small payments, they make it easier psychologically.

Conclusion: Debt Is a Financial Problem, Not a Moral Failure

There is a very simple message in this article and it’s the most important one. Being in debt is not a bad thing. Doesn’t make you a failure. It turns you into a guy who has a monetary trouble. The sense of being unworthy as a result of your culture, your society, your previous life because they are saying you are worthless because you don’t have money. This equation is not true. You’re not valuable as a human being by the amount of money you have or your credit score. Being in debt does not mean you are a bad or unhappy parent, a bad friend, an inefficient employee, or bad person, worthy of peace. Getting out of debt can be a long and arduous journey, but the first step is the most important. Don’t be silent, stop suffering. Speak to someone. Don’t let your finances affect your mental well-being.

Hybrid Cars: The Smartest Financial Choice Driving Kenyan Mobility Today – Kenya Financial Updates

Discover more from Kenya Financial Updates

Subscribe to get the latest posts sent to your email.

{kind=link}

{kind=link}